Transfer Pricing in Colombia is the mechanism used by the Colombian Tax Authority (DIAN) to ensure that transactions between related parties — for example, a foreign parent company and its Colombian subsidiary — are carried out at market value, just as they would be between independent entities.

The main goal of the Transfer Pricing Regime is to prevent profit shifting to low-tax jurisdictions and ensure that income is properly taxed in Colombia.

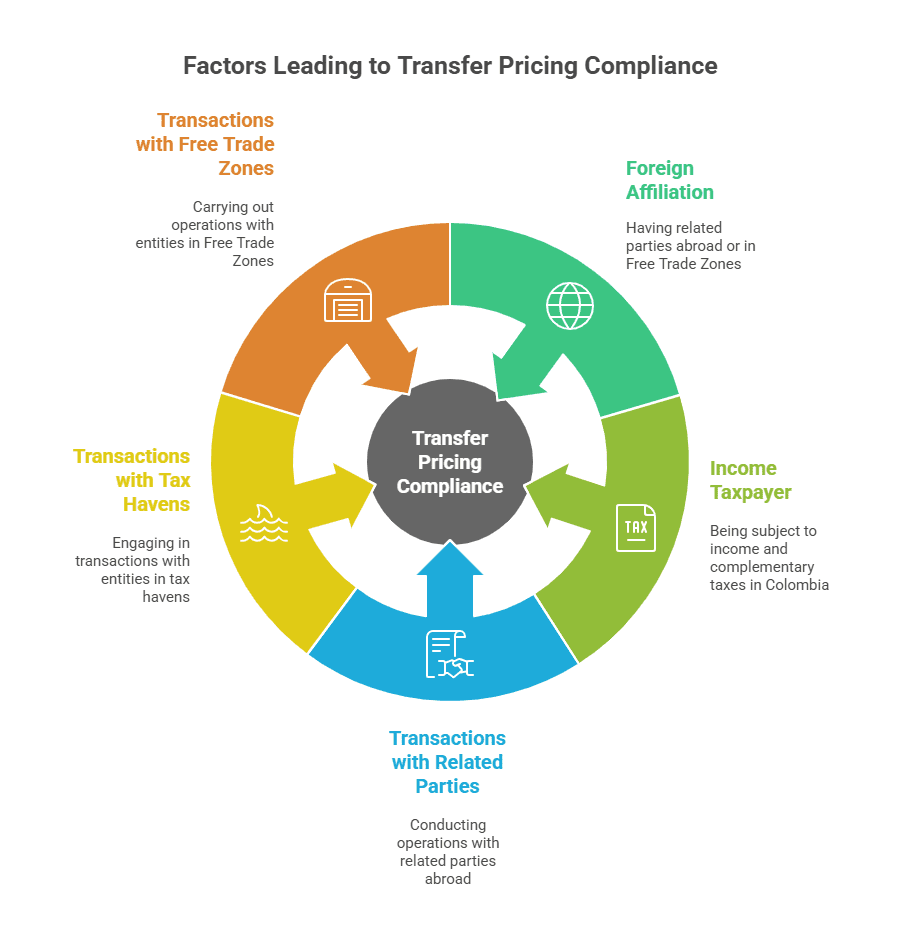

Who Is Obliged to Comply?

Companies and individuals must comply with the Colombian Transfer Pricing rules if they meet the following conditions:

- They are income tax payers in Colombia.

- They have related parties abroad or related entities located in Free Trade Zones.

- They conduct transactions during the fiscal year with any of the following:

- Foreign related parties.

- Entities or individuals located in tax havens.

- Related parties located in Colombian Free Trade Zones.

Main Transfer Pricing Obligations and Thresholds in Colombia

| OBLIGATION | APPLIES TO | MAIN THRESHOLD | DETAILS AND NOTES |

|---|---|---|---|

| Transfer Pricing Informative Return | Income taxpayers with a gross equity equal to or greater than 100,000 UVT or gross income equal to or greater than 61,000 UVT, who carry out transactions with foreign-related parties or entities located in Free Trade Zones. It also applies to taxpayers operating with non-cooperative jurisdictions or preferential tax regimes, regardless of the transaction amount. | 100,000 UVT (equity) / 61,000 UVT (income) / 10,000 UVT (for transactions with non-cooperative jurisdictions) | Includes, when applicable, the Country-by-Country (CbC) notification within the form. |

| Supporting Documentation – Local File | Taxpayers required to file the informative return and who carry out transactions with related parties for 45,000 UVT or with non-cooperative jurisdictions for 10,000 UVT. | 45,000 UVT / 10,000 UVT | Must include detailed information on specific transactions, functions, assets, and risks (FAR analysis). |

| Supporting Documentation – Master File | Taxpayers that file the Local File and belong to a multinational group (entities with a fiscal presence in more than one jurisdiction). | — | Summarizes the group structure, value chain, and transfer pricing policy of the multinational group. |

| Country-by-Country Report (CbCr) | Parent companies of multinational groups or those designated as such, with consolidated income of 81,000,000 UVT in the previous year. | 81,000,000 UVT | Must be filed electronically; notification is required even if the entity has no other formal obligations. |

| Attribution Study | Branches and permanent establishments of foreign companies in Colombia. | — | Internal document describing functions, assets, and risks; only submitted to DIAN upon request (Article 20, Tax Code). |

UVT Value Reference

- For 2024: COP 47,065

- For 2025: COP 49,799

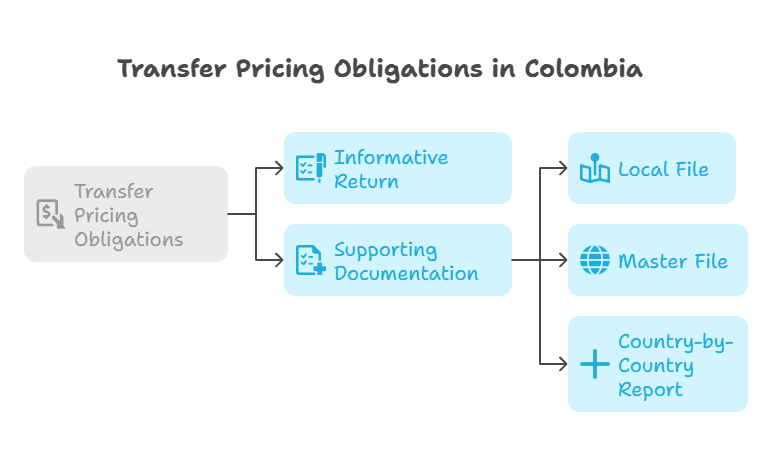

What Documents Must Be Filed?

Transfer Pricing obligations in Colombia are divided into two main levels:

- Informative Return: A general report of transactions with foreign related parties (DIAN Form 120).

- Supporting Documentation: Technical evidence demonstrating that the transactions were conducted at arm’s length (market value):

- Local File: Provides detailed information on the Colombian company’s intercompany transactions.

- Master File: Describes the structure of the multinational group and its global transfer pricing policy.

- Country-by-Country Report (CbCr): Applies only to large multinational groups.

Non-Compliance Risks

Failing to file or filing the return or documentation late can lead to penalties ranging from 0.4% to 4% of the total value of the transactions, with limits up to 20,000 UVT (Articles 260-11 and 651 of the Colombian Tax Code).

In addition to monetary penalties, the DIAN may adjust the declared prices or profit margins and recalculate income tax, resulting in higher taxes due, interest payments, and potential tax disputes.

Nieto Lawyers’ Recommendation

Even if your company is not formally required to file Transfer Pricing documentation, it is strongly recommended to maintain technical support for intercompany transactions, particularly in marketing, healthcare, pharmaceutical, and technology sectors, where operations often involve intangibles or specialized services.

At Nieto Lawyers, we help your company determine whether it is subject to the Transfer Pricing regime, prepare the required documentation, and prevent DIAN sanctions through smart and strategic compliance.

Does Your Company Exceed the Transfer Pricing Thresholds?

At Nieto Lawyers, we help you:

- Diagnose your Transfer Pricing obligations.

- Prepare DIAN-compliant documentation.

- Avoid costly tax penalties.

Book a free tax compliance review here:

WhatsApp

WhatsApp